LOVE, MARRIAGE… AND SEPARATE CHECKING ACCOUNTS?

June is wedding season—but it’s also anniversary season.

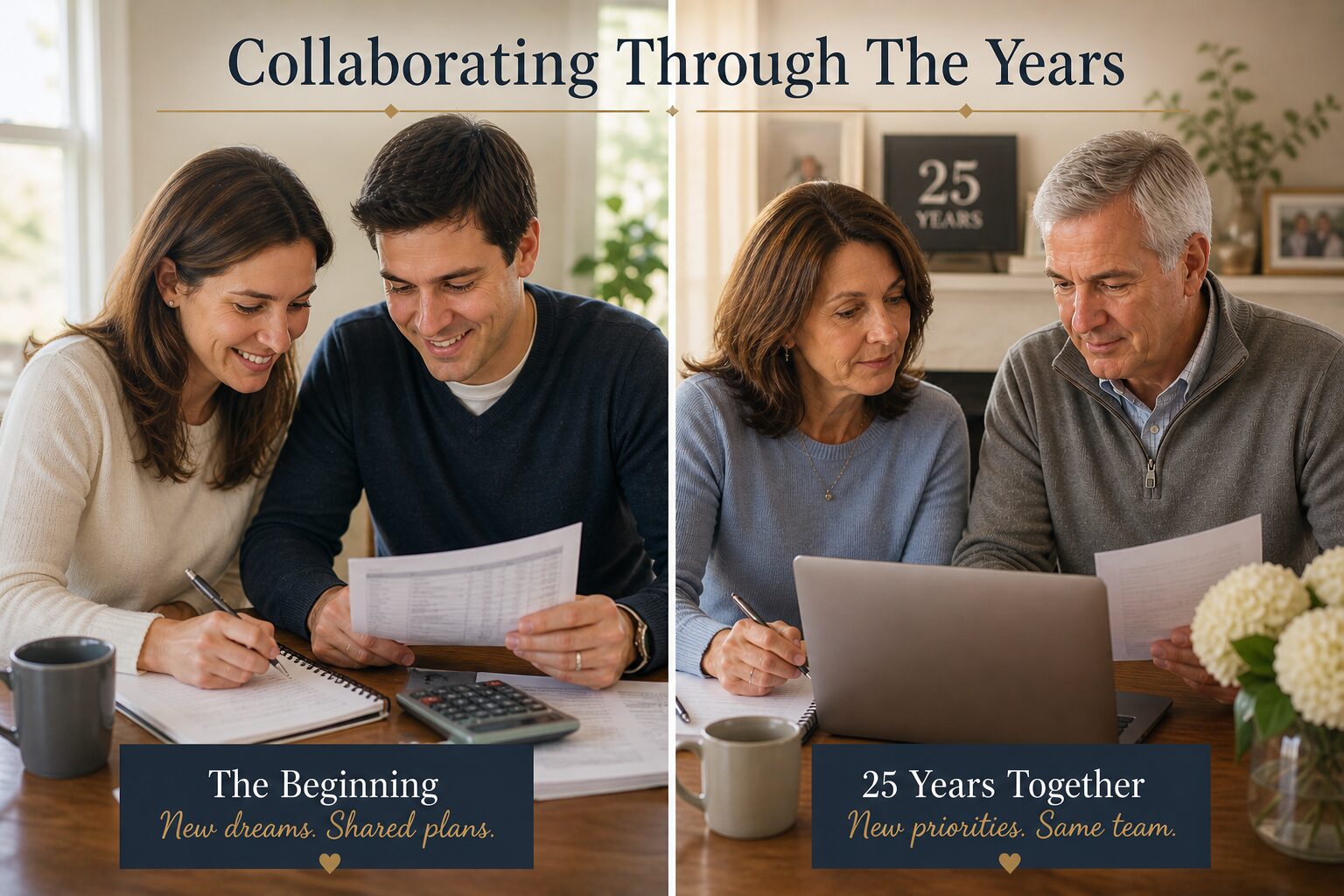

For some, it’s the start of a marriage, complete with honeymoons and newly combined (or not-so-combined) finances. For others, it’s a chance to celebrate 10, 20, or even 30+ years together—and maybe reflect on how their financial lives have evolved along the way.

And whether you’re just starting out or have been managing money together for decades, one question tends to come up at some point:

“Should we combine everything… or keep things separate?”

The honest answer: there is no universally “right” way to do this. There is only the way that works best for both of you.

The Three Common Approaches

Most couples fall into one of three buckets:

1. Fully Combined

All income goes into shared accounts. All expenses are paid together.

• Simple and transparent

• Encourages a “team” mindset

• Can reduce administrative headaches

But… it can also feel restrictive if one partner values independence.

2. Fully Separate

Each spouse maintains their own accounts and splits expenses.

• Preserves autonomy

• Works well for second marriages or established financial habits

• Can reduce conflict over spending differences

But… it requires coordination—and sometimes awkward “who pays for what” conversations.

3. The Hybrid Approach

A shared account for household expenses, plus individual accounts for personal spending.

• Balances teamwork and independence

• Reduces friction over discretionary purchases

• Allows both partners to maintain some financial flexibility

This approach can offer flexibility and balance, but it still requires clear communication and ongoing coordination.

The Real Issue Isn’t Structure—It’s Visibility and Communication

Here’s what matters far more than how you structure accounts:

• Do you have shared goals?

• Are you both clear on income, expenses, and debt?

• Have you agreed on spending expectations?

• Are you working toward the same long-term plan?

We’ve seen couples with completely separate finances thrive…And couples with fully combined finances struggle.

The difference is usually not the structure itself—it’s whether both partners understand and stay engaged with the plan.

How to Decide What’s Right for You

Whether you’re newly married, just back from your honeymoon, or celebrating your 5th, 15th, or 25th anniversary, here are three simple steps:

1. Start with a judgment-free conversation

Talk about money histories, habits, and preferences. No scorekeeping.

2. Define “fair”—not necessarily “equal”

Especially when incomes differ, fairness doesn’t always mean 50/50.

3. Create a system—and schedule time to review it

What works today may need adjusting later—especially after big life moments.

At a minimum, couples should sit down together at least twice a year to review their finances. This is especially important if one partner handles the day-to-day money decisions. A simple check-in helps ensure both people stay informed, aligned on priorities, and comfortable with how things are being managed. An anniversary can actually be a great built-in reminder—slightly less exciting than dinner reservations, but potentially far more valuable.

One More Thing…

Whether you combine everything, keep things separate, or land somewhere in between, the goal is the same: clarity, transparency, and a system that both partners understand and feel good about.

If you’re not sure whether your current system is helping—or quietly creating stress—it may be worth a conversation with a Certified Financial Planner® who can help you both see the bigger picture. A thoughtful conversation now, guided by a neutral and knowledgeable CFP®, can prevent confusion, frustration, or surprises down the road.