A “BIG, BEAUTIFUL” CHANGE FOR 2025 TAXES

Just when you thought Washington had run out of adjectives, along came the Big Beautiful Bill—and, surprisingly, this one might actually live up to its name—at least where your 2025 taxes are concerned.

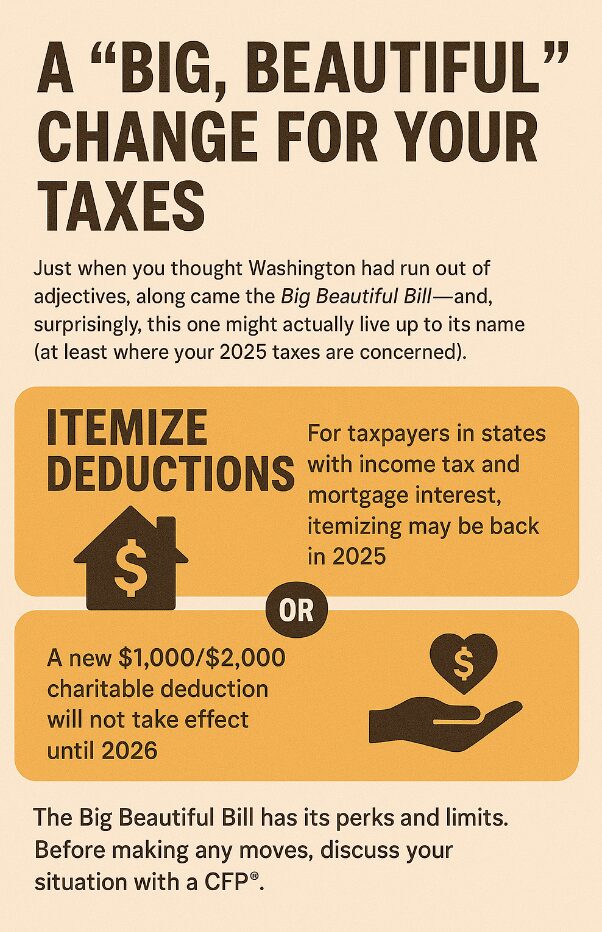

One of the most talked-about features of this new legislation is its impact on itemized deductions—something many of my clients haven’t seen since the 2017 Tax Cuts and Jobs Act (TCJA) nearly doubled the standard deduction and made itemizing a rare luxury. But 2025 could mark a turning point, especially if you live in a state that collects income tax, you pay property taxes, and you pay mortgage interest.

Why This Matters

For the past several years, most taxpayers took the standard deduction because it simply offered a bigger break. Even homeowners in high-tax states found that the $10,000 cap on state and local tax (SALT) deductions limited their ability to itemize.

Under the Big Beautiful Bill, that cap is being loosened—or in some cases removed, making it far more likely that taxpayers in states like New York, Massachusetts, Maine, and others will again find it worthwhile to itemize. Combine state income taxes, mortgage interest, charitable donations, and perhaps some medical expenses, and suddenly that old Schedule A starts looking attractive again.

In short: Itemizing might be back on the table—and that means more flexibility in how you manage deductions and charitable giving strategies.

But What If You Don’t Pay State Income Tax Or Have Other Itemized Deductions?

Don’t worry—the Big Beautiful Bill didn’t forget you. For taxpayers in states like Florida, Texas, and Tennessee—where there’s no state income tax to deduct—itemizing will likely still be out of reach for most households. And even if you live in a state with an income tax, if you don’t have mortgage interest or other significant deductions, you may still find the standard deduction to be the better deal.

However, there’s a new consolation prize, but you do have to wait until 2026 to receive it: a “universal” charitable deduction of up to $1,000 for single filers and $2,000 for married couples filing jointly, even if you don’t itemize. That’s a nice incentive to keep giving to your favorite charities, and it’s a welcome acknowledgment that generosity shouldn’t depend on your ZIP code.

The Fine Print – Because There’s Always Fine Print

Of course, nothing in the tax code is ever simple. There are income limits, qualifying donation rules, and timing requirements that can affect whether these new deductions apply to you—and how much you can actually claim. And that’s where professional guidance becomes crucial.

The difference between a well-planned tax strategy and a missed opportunity often comes down to a few key decisions made. Adjusting your charitable giving, revisiting your mortgage strategy, or even timing state tax payments could make a meaningful difference in what you owe—or what you save—next April.

The Bottom Line

The Big Beautiful Bill may not make your tax return beautiful, but it could make it more interesting. If you’ve been defaulting to the standard deduction year after year, it’s time to take a fresh look at whether itemizing could save you money—or whether the new charitable deduction could enhance your giving in a tax-smart way.

Every taxpayer’s situation is unique, and the new rules add both opportunities and complexity. Before making any year-end tax moves, it is important to work with a Certified Financial Planner® who will help you keep more of your hard-earned money working for you and not just funding Congress’s next beautifully named bill.